In Wyoming, property taxation is divided into three tiers, depending on the type of property:

Mineral Production: Taxed at 100% of productive value

Industrial Property: Taxed at 11.5%

All Other Property: Including commercial, agricultural, and residential properties, taxed at 9.3%

- Property taxes in Wyoming primarily fund local government services and schools. Community colleges receive around 4% of the property tax revenue in their county.

- The residential sector provides the most predictable and steady source of assessed value.

In the 2026 General Election, Wyoming voters will consider the first citizen initiative to reach the ballot in 30 years, and it could significantly reduce local government revenues — including counties, cities, K–12 schools, and community colleges — because the measure does not require any state backfill.

WY Property Tax FAQ

What do property taxes fund in Wyoming?

In Wyoming, property taxes are utilized to support local communities, primarily funding local government services and schools. The dollars do not flow to the state’s general fund. Here’s a breakdown of how property tax revenue is typically allocated. Note that percentages can vary slightly from county to county.

- Schools: Approximately 69% of property taxes go towards funding local K12 schools. This portion is pooled into a common account and then redistributed to all counties.

- Counties: Around 17% of property taxes fund county operations, including the sheriff’s office, road and bridge maintenance, and other county services.

- Special Districts: About 8% goes to special districts that provide local services such as rural fire departments, weed and pest control, rural hospitals, soil conservation districts, senior citizen centers, and solid waste districts.

- Cities and Towns: Cities and towns receive about 2% for services like water and sewer, cemeteries, and museums.

- Community Colleges: If there is a community college in the area, it receives around 4% of the property tax revenue.

How do Wyoming’s property taxes rank as compared to surrounding states?

Wyoming’s residential property taxes are low compared to surrounding states. Here’s a quick comparison.

-

Wyoming: The effective tax rate is approximately 0.645%, with an average tax bill of $1,780 for a median-valued home.

-

Colorado: The effective tax rate is around 0.519%, with an average tax bill of $2,808 for a median-valued home.

-

Idaho: The effective tax rate is about 0.622%, with an average tax bill of $2,864 for a median-valued home.

-

Montana: The effective tax rate is approximately 0.932%, with an average tax bill of $2,704 for a median-valued home.

-

Nebraska: The effective tax rate is around 2.006%, with an average tax bill of $4,251 for a median-valued home.

Has the Legislature Offered Meaningful Property Tax Relief?

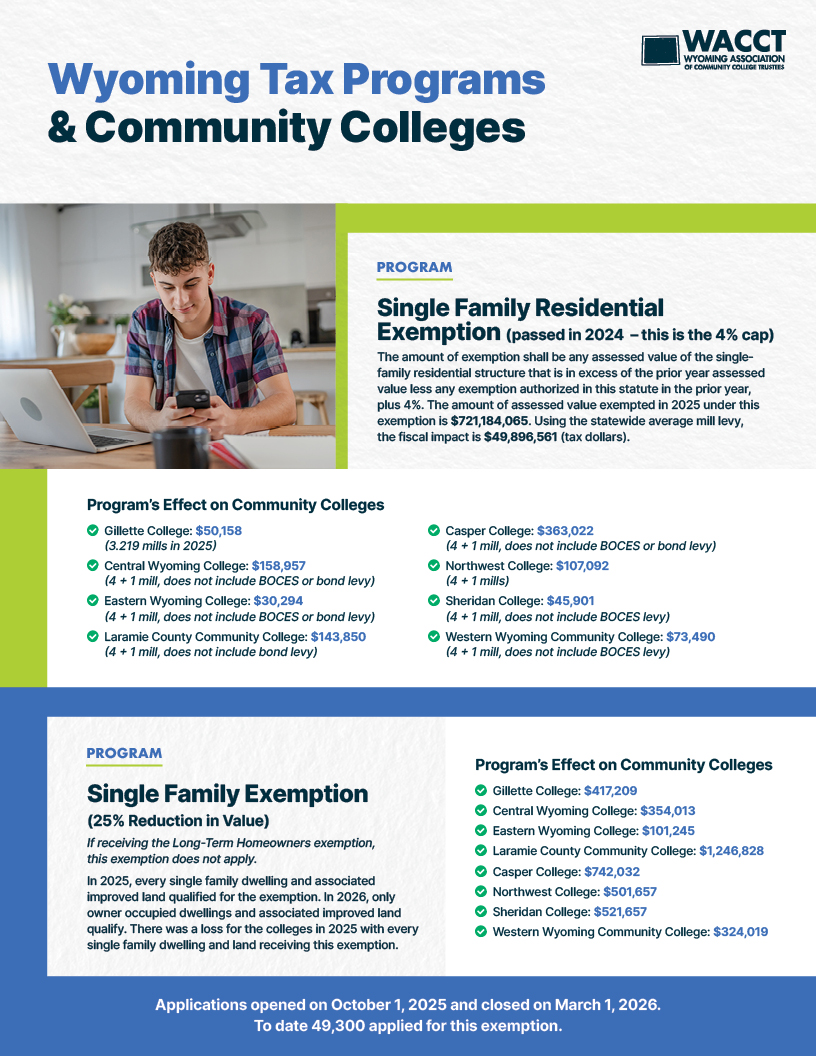

Single Family Residential Exemption (passed in 2024 – this is the 4% cap)

-

-

-

- The amount of exemption shall be any assessed value of the single‐family residential structure that is in excess of the prior year assessed value less any exemption authorized in this statute in the prior year, plus 4%. The fiscal impact of this exemption is estimated to be $300M. Not backfilled.

-

-

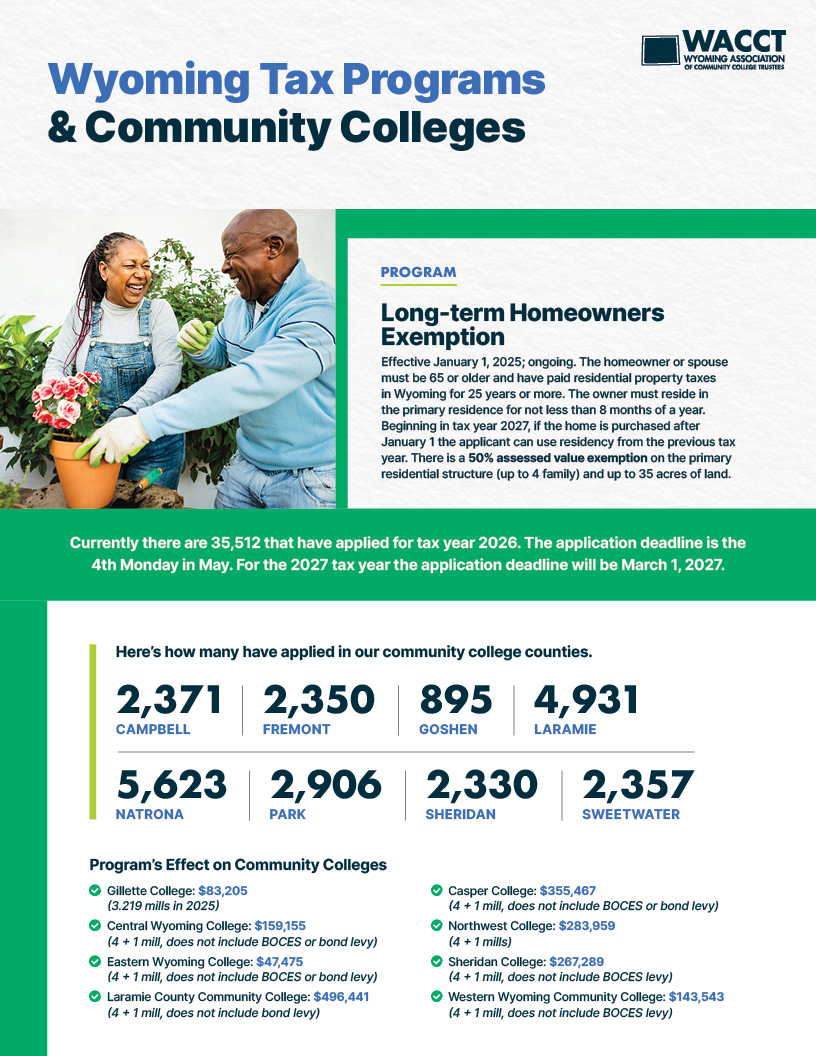

Long-term Homeowners Exemption

-

-

-

- Effective January 1, 2025, ongoing.

- Owner or spouse must be 65 or older and have paid residential property taxes in Wyoming for 25 years or more. Owner must reside in the primary residence for not less than 8 months of a year.

- 50% assessed value exemption on the primary residential structure and up to 35 acres of land.

- To date, approximately 18,000 properties have already qualified, and it is anticipated that a total of 25,000 may qualify. Not backfilled. The fiscal impact is not yet known.

-

-

Property Tax Refund Program

-

-

-

- The program has been expanded in the last several years so that more people can qualify. It is only available if funds are appropriated by the Legislature (it has been funded since 2022) and was yet expanded again in the 2025 session.

- Application available at the County Treasurer’s office or from the Department of Revenue website.

- Must have paid property tax timely.

Household income must be less than the greater of 145% of the county or state median household income. - Household assets (excluding the house, a car for each adult household member, and IRA and other pension funds) must be worth less than $156,900 per adult household member.

-

-

Property Tax Deferral Program

-

-

-

- Available at participating County Assessor’s offices (currently only Teton County).

- Must be the principal residence on a parcel of land of less than 40 acres.

- Owner must have limited income, be over 62 years old or handicapped (as determined by the Social Security Administration), and have purchased the property 10 years prior to applying for deferral of taxes.

- Up to ½ of property taxes on a qualifying principal residence can be deferred.

-

-

Veteran’s Property Tax Exemption Program

-

-

-

- Available at local County Assessor’s and/or County Treasurer’s offices (currently, only Teton County).

- Honorably discharged veterans of WWI, WWII, Korea, Vietnam, or those awarded the armed forces expeditionary medal or other authorized service or campaign medal indicating service in any armed conflict in a foreign country.

- Surviving spouses of qualifying veterans and certain disabled veterans may also be eligible.

- Provides a property tax exemption of $6,000 in assessed value against real or personal property. (the Legislature doubled the benefit in the 2024 budget session)

-

-

County Optional Property Tax Refund Program

-

-

-

- Albany, Lincoln, Converse, Teton, and Sublette

- Only if funded at the county level.

- Property tax paid timely; household income and asset limits determined by the county; resident of Wyoming for the past 5 years.

-

-

What Bills Passed This Legislative Session?

For community colleges, the key issue was the cumulative impact of earlier property tax cuts on local mill revenue, combined with the rising cost of delivering high‑quality education. The Wyoming Community College Commission estimated that existing property tax relief measures would reduce local mill revenue by roughly $16–17 million across the system over the biennium, even as colleges requested additional state funding just to keep pace with inflation.

WHAT IS HB 45?

HB 45 is the only bill related to property tax relief to pass in the 2026 legislative session.

HB 45 – Long Term Homeowner Tax Exemption explained:

-

-

-

- Raises the long-term homeowner exemption amount and updates eligibility rules for homeowners who have lived in their primary residence for the required number of years.

- Applies the 50% exemption only to the first $3 million of a home’s fair market value, creating a clear cap on the benefit.

- Moves the application deadline to March 1 and allows homeowners who already qualify to renew annually through a simple confirmation rather than a full re-application.

- Clarifies definitions, including “primary residence,” to ensure consistent administration across counties.

- Repeals the program’s sunset date, making the exemption permanent unless changed by future legislation.

- Prevents dual benefits by prohibiting homeowners from claiming this exemption if a separate voter-approved homeowner exemption initiative goes into effect.

-

-

What Impact Will the Ballot Initiative Have?

As WACCT has noted, there is currently no trigger bill in place for the 25% homeowner’s exemption—lawmakers discussed creating one but did not pass it—meaning the 25% exemption and the citizen initiative can both be used together under existing law; however, homeowners who qualify for the long‑term homeowner’s exemption may not claim both that exemption and the initiative under HB 45 (2024)

WY Tax Property Landscape

In this WACCT webinar, participants welcome Hank Hoversland of the Wyoming Taxpayers Association to review and discuss Wyoming’s property tax landscape and recent legislative changes. The session provides insights into how property tax policy impacts community colleges, education funding, and taxpayers across the state.

WY Tax Property Benefits

The Cowboy Family is intended to deliver a deep dive into the average state taxes Wyoming citizens pay and the benefit of services they receive, and provide transparency regarding what individual benefits the Wyoming tax structure provides. Here, taxes paid are equated with services received by the Cowboy Family.

Property Tax State by State

This map compares effective tax rates across states, showing Wyoming as the 13th lowest in the nation.

Property Tax Relief Resource Center

WACCT

Percentage Residential and Minerals by County

COUNTY |

RESIDENTIAL |

MINERALS |

TOTAL VALUE |

|---|---|---|---|

Campbell |

303,218,367 6.26% |

3,797,719,892 78.46% |

4,840,295,046 |

Fremont |

294,157,135 42.25% |

199,314,069 28.63% |

696,250,090 |

Goshen |

83,656,256 29.70% |

2,181,794 0.77% |

281,671,517 |

Laramie |

913,243,035 33.69% |

832,192,459 30.70% |

2,710,697,112 |

Natrona |

587,435,726 41.24% |

295,362,060 20.74% |

1,424,308,252 |

Park |

420,986,736 49.43% |

261,716,499 30.73% |

851,601,842 |

Sheridan |

431,127,559 69.22% |

1,695,844 0.27% |

622,875,881 |

Sweetwater |

237,820,562 10.26% |

1,241,710,949 53.56% |

2,318,423,330 |

*Percentage of Assessed Value Residential vs Minerals. 2025 Assessed Values from Annual Report.

Percentage Residential and Minerals by County

COUNTY |

RESIDENTIAL (R) MINERALS (M) & TOTAL VALUE (T) |

|---|---|

Campbell |

(R) 303,218,367 (M) 3,797,719,892 (T) 4,840,295,046 |

Fremont |

(R) 294,157,135 (M) 199,314,069 (T) 696,250,090 |

Goshen |

(R) 83,656,256 (M) 2,181,794 (T) 281,671,517 |

Laramie |

(R) 913,243,035 (M) 832,192,459 (T) 2,710,697,112 |

Natrona |

(R) 587,435,726 (M) 295,362,060 (T) 1,424,308,252 |

Park |

(R) 420,986,736 (M) 261,716,499 (T) 851,601,842 |

Sheridan |

(R) 431,127,559 (M) 1,695,844 (T) 622,875,881 |

Sweetwater |

(R) 237,820,562 (M) 1,241,710,949 (T) 2,318,423,330 |

*Percentage of Assessed Value Residential vs Minerals. 2025 Assessed Values from Annual Report.

Wyoming Association of Community College Trustees Handbook

Wyoming Tax Programs & Community Colleges Single Family Residence Programs

Wyoming Tax Programs & Community Colleges Long-term Homeowners Program

Wyoming Department of Revenue

Wyoming County Commissioners Association

Wyoming Taxpayers Association

The Tax Foundation

Learn More About Wyoming’s Community Colleges